Parents

Research

Apr 1, 2026

Getting Smaller is Actually Better for Nuclear Energy

Andrew Z

Research Fellow

The Dream of Old

For much of the 20th century, nuclear power was seen as the future of energy for the United States. At its core, nuclear power relies on fission, the splitting of uranium-235 atoms. When these atoms split, they release enormous amounts of heat. In a commercial reactor, that heat is used to boil water, produce steam, spin turbines and ultimately generate electricity without direct carbon emissions.

In 1960, Yankee Rowe, the first fully commercial pressurized water reactor designed by Westinghouse, began operating. That same year, Dresden 1, a boiling water reactor designed by General Electric and based on work from Argonne National Laboratory, also came online. By the late 1960s, utilities were placing orders for reactors exceeding 1000 MWe, and construction surged. Pressurized water reactors and boiling water reactors became the backbone of the US fleet and remain the only two designs built commercially in the country.

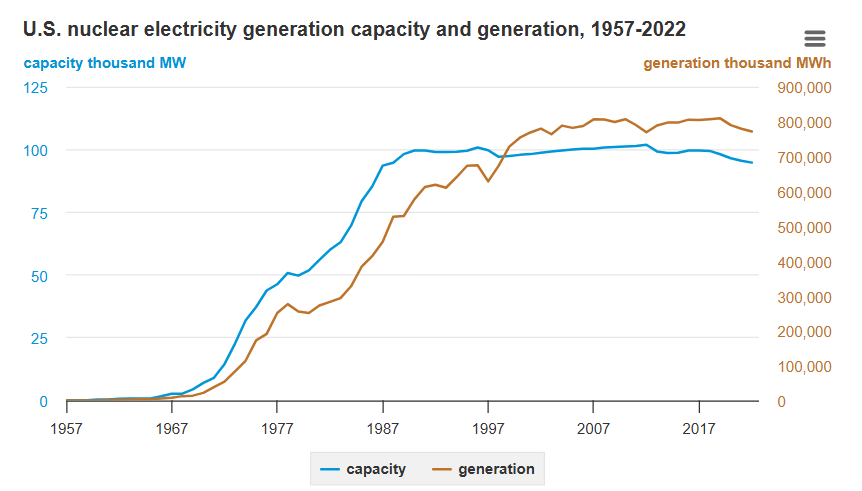

Most of the reactors operating today were constructed between 1967 and 1990. As of 2023, the United States had 93 operating commercial nuclear reactors in 28 states, with an average age of about 42 years. The fleet once reached 112 operating reactors, and total net summer generating capacity peaked in 2012 at roughly 102,000 MW. Since then, a series of retirements has reduced both the number of reactors and total capacity, which stood at 94,765 MW in 2022.

Source: Energy Information Administration

Today, nuclear energy generates nearly 20% of all U.S. electricity and roughly 55% of the nation’s carbon-free electricity. Yet its share of total commercial energy has fallen to its lowest level in 25 years as of 2023. The US nuclear industry now stands at an inflection point: built on decades-old infrastructure, still delivering reliable clean power at scale, but facing the realities of plant retirements and a rapidly changing energy landscape.

Despite current trends in nuclear energy, three trends that revolve around small modular reactors (SMRs) will re-pivot the industry: the development and introduction of SMRs themselves; surging electricity demand from AI and data centers that provides a use case for SMRs; and the expansion of the domestic nuclear fuel supply chain used by SMRs. All of these should interest retail investors.

Just Like Legos

One of the biggest constraints for nuclear energy cost and construction time. Large conventional reactors are massive infrastructure projects that often take years longer and billions more dollars than initially projected. A recent example is Southern Company’s Vogtle expansion in Georgia, which brought the first new US reactors online in decades but finished roughly seven years behind schedule at a total cost exceeding $30 billion. These challenges have made utilities hesitant to commit to another wave of gigawatt-scale builds.

Small modular reactors, or SMRs, are designed to solve this problem. Traditional nuclear reactors typically produce around 1000 MWe or more per unit, whereas SMRs are defined by their smaller electrical output, generally less than 300 MWe. Their smaller capacity allows quicker deployment and deployment in settings where large plants may not be practical, such as remote communities or regions with limited grid infrastructure.

Modularity is the core innovation. Both large and small nuclear reactors increasingly rely on modular construction techniques, assembling major components in specialized facilities before transporting them to the plant site. However, SMRs take this concept several steps further. Entire reactor modules are designed for factory fabrication under controlled conditions. Designers envision serial production, similar to an assembly line, where standardized units are manufactured repeatedly to achieve economies of series, much like in the aerospace industry. These prefabricated modules are then shipped to the site for on-site assembly, reducing construction complexity, improving quality control, shortening timelines, and potentially lowering overall costs. SMRs are also built for scalability. Utilities can deploy reactors incrementally, adding modules as electricity demand rises rather than committing to a single multibillion-dollar project upfront. This staged approach reduces financial risk and offers customers greater flexibility.

Executives across the nuclear industry widely expect that SMRs will reach commercial scale in the 2030s. The United States remains a global hub for SMR development, supported by favorable policies and available funding. If successfully deployed, SMRs could represent up to 15% of global uranium demand by 2040. In the near term, there is the possibility that 3 SMRs could be connected to the US grid by 2034, with another 5 or 6 connections following soon after.

While still early in commercialization, SMRs offer a pathway to address the cost, scale, and deployment challenges that have constrained traditional nuclear expansion. As SMRs approach that scaling phase, new demand drivers for nuclear energy are emerging. Coal-to-nuclear switching presents one opportunity, where retiring coal plants could be repurposed with advanced nuclear technology. At the same time, the rapid growth of AI and data centers is increasing demand for firm, carbon-free electricity, a profile that aligns closely with nuclear power. SMRs are also gaining traction for remote operations such as oil and gas exploration, where reliable power is essential and grid access may be limited.

What Would I do without Chat?

The scale and speed of the AI revolution in particular have created a massive energy demand profile that increasingly aligns with nuclear power’s core strengths. Training advanced AI models requires tens of thousands of GPUs running continuously for weeks or even months, consuming huge amounts of electricity. Globally, AI data centers use more than 400 TWh of electricity per year. With AI workloads expanding at unprecedented rates, projections suggest this could more than double to nearly 1000 TWh (roughly equivalent to the entire annual power consumption of a G7 country) annually within the next decade.

Many firms have pledged to power their operations with low-carbon sources, yet renewable energy alone has limitations. Solar and wind are inherently weather-dependent, which creates intermittency challenges. Even at peak output, they may only meet about 80% of a data center’s demand profile, and they require storage or backup systems to ensure reliability. Data centers, by contrast, require uninterrupted, 24/7 electricity. Nuclear power offers zero direct carbon emissions and delivers consistent baseload output, making it uniquely positioned to satisfy the combined requirements of low-carbon generation, round-the-clock reliability, high power density, grid stability and scalability.

Goldman Sachs estimates that 85 to 90 GW of new nuclear capacity may be required by 2030 to meet projected data center demand. Yet only about 10% of that capacity is currently expected to be available, highlighting a significant supply gap. Despite these barriers, corporate confidence in nuclear is rising. Rather than relying solely on conventional large reactors, many companies are turning toward small modular reactors as a more flexible solution. SMRs, being smaller and modular by design, can potentially be located closer to data centers, reducing transmission losses and, in some designs, lowering cooling water requirements. While the first SMRs are not expected to be operational until 2029, major tech corporations have already signed development agreements to accelerate deployment.

Google, Meta, and Amazon have joined 14 of the world’s largest banks and financial institutions in pledging to triple global nuclear capacity by 2050. Constellation Energy captured headlines when it announced the restart of Three Mile Island Unit 1, now renamed the Crane Clean Energy Center, in partnership with Microsoft. Google signed an agreement with Kairos Power to purchase 500 MW of electricity. Amazon has invested $500 million in X-energy and announced plans targeting 5 GW of nuclear capacity. Meta has issued a request for proposals seeking 4 GW of nuclear power.

Taken together, AI-driven electricity demand is elevating nuclear power, particularly SMRs, from a legacy asset to a strategic necessity.

More Uranium Please

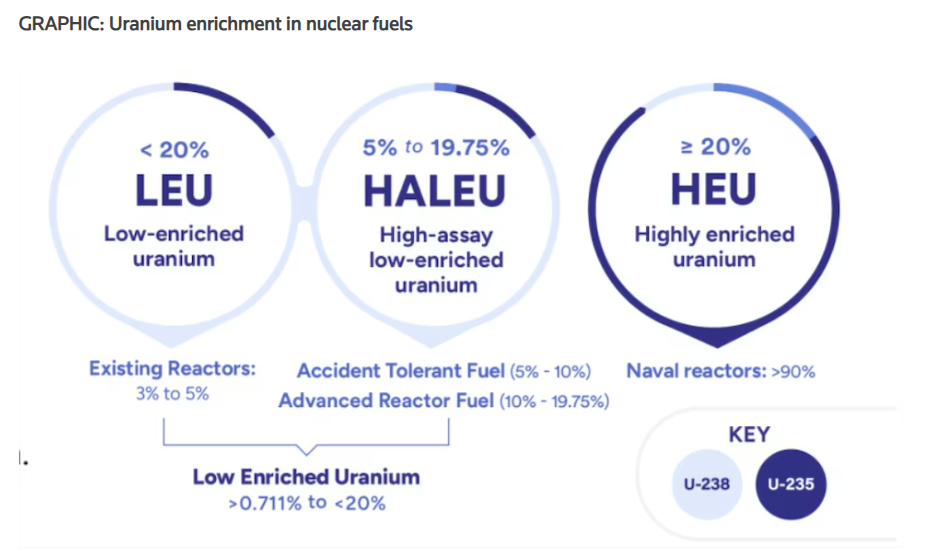

Behind every nuclear reactor is a less visible but equally critical system: the fuel supply chain. Nuclear fuel begins as natural uranium, which contains about 0.7% fissile uranium-235 (U-235), the isotope responsible for sustaining the fission process. To function in a commercial reactor, uranium must be enriched, increasing the concentration of U-235. Most existing nuclear plants operate using low-enriched uranium (LEU), which typically contains between 3.5% and five percent U-235. This enrichment is commonly achieved by converting uranium into gaseous uranium hexafluoride and processing it through centrifuges.

SMRs often depend on high-assay low-enriched uranium (HALEU), which contains between five percent and 20% U-235. The shift toward HALEU significantly alters fuel supply dynamics. It introduces new production requirements at a time when the domestic enrichment industry remains limited.

Source: Reuters

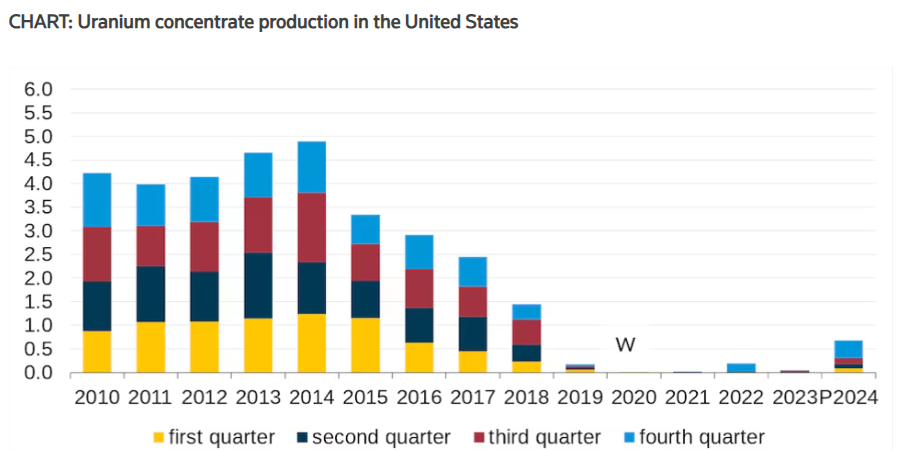

The United States was once a global leader in nuclear fuel production during the Cold War. However, over the following decades, the domestic industry contracted as cheaper imports from Russia, France, the Netherlands and the United Kingdom captured market share. Today, the US has only one large-scale LEU enrichment plant, owned by Urenco, and its capacity is sufficient to meet roughly one-third of the enrichment needs of US commercial nuclear power plants. In 2023, US nuclear operators used 32 million pounds of imported uranium concentrate (U3O8) and only 0.5 million pounds of domestically produced U3O8. Imports accounted for 99% of the uranium concentrate used to make nuclear fuel that year.

Source: Reuters

This reliance has become more problematic as demand shifts toward HALEU. Russia has historically been the sole commercial producer of HALEU. Following Russia’s invasion of Ukraine, the US imposed strict annual limits on imports of Russian uranium, with a full ban scheduled to take effect in 2028. At the same time, the Department of Energy projects that US demand for HALEU could reach 50 metric tons per year by 2035, with additional increases thereafter. Yet Centrus Energy, currently the only US company capable of producing HALEU, has capacity of approximately 1 metric ton per year. Without rapid expansion, limited domestic supply could constrain SMR deployment in the 2030s.

Fortunately, in January, the US government announced a $2.7 billion allocation to support three nuclear fuel developers, aimed at revitalizing domestic enrichment and easing potential shortages for SMRs and advanced reactors. Under the award, three companies will each receive $900 million to expand supply chain capacity. American Centrifuge Operating, a subsidiary of Centrus Energy, and General Matter will use funds to increase domestic enrichment capability for HALEU. Orano Federal Services will focus on expanding domestic low-enriched uranium production. Although near-term supply risks remain, this federal intervention directly addresses one of the most significant bottlenecks facing advanced reactors. By strengthening domestic enrichment capacity, policy support is laying the groundwork for SMRs to scale more rapidly and reliably in the next decade.

What to Consider

The structural push from AI-driven electricity demand, the commercialization of SMRs, and the rebuilding of the domestic fuel supply chain are reshaping the nuclear energy industry, making it much more interesting for retail investors in the coming years. Investors may consider:

- Companies focused on uranium mining and raw fuel supply

- Cameco (CCJ)

- Denison Mines (DNN)

- Uranium Energy Corp (UEC)

- Companies expanding enrichment and fuel capabilities

- Centrus Energy (LEU)

- Companies supplying nuclear components and technology

- BWX Technologies (BWXT)

- NuScale Power (SMR)

- Utilities with nuclear exposure and expansion potential

- Constellation Energy (CEG)

- Xcel Energy (XEL)

- Duke Energy (DUK)

- NextEra Energy (NEE)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.