Parents

Research

Feb 18, 2026

A More Stable(coin) Path To The Moon

Andrew Z

Research Fellow

A More Stable(coin) Path To The Moon

Sablecoins? You mean Bitcoin?

Cryptocurrencies are a type of digital money you can send online. As opposed to traditional currency, there is no government issuing crypto and no financial institution facilitating each transaction of crypto. Given its decentralized nature, crypto offers a new, faster way of handling money that can work across borders that can keep working even if one institution fails. The most well-known cryptocurrency, and most widely-used for transactions, is Bitcoin. However, cryptocurrencies can have wild price swings, making them hard to use for everyday spending.

Stablecoins are a type of cryptocurrency, but they’re different from coins like Bitcoin because their price doesn’t jump up and down all the time. Instead, they are designed to stay at a steady value (usually $1 per coin). To make that possible, each stablecoin is tied (or “pegged”) to the US dollar or other financial assets. In practice, stablecoins work using a mint-and-redeem mechanism:

- If someone gives a stablecoin company 1 real US dollar, the company creates (or mints) 1 new stablecoin for that person.

- Later, if that person wants their real dollar back, the company takes away (or burns) the stablecoin and returns $1 from the money it has saved.

Because of this system, stablecoins can act like digital dollars you can send instantly: useful for buying things, sending money to friends or using in crypto apps without worrying about big price swings. The 2 biggest stablecoins — Tether (USDT) and Circle’s USD Coin (USDC) — make up about 93% of all stablecoins in the world, and both are backed by the US dollar.

A Stellar Record

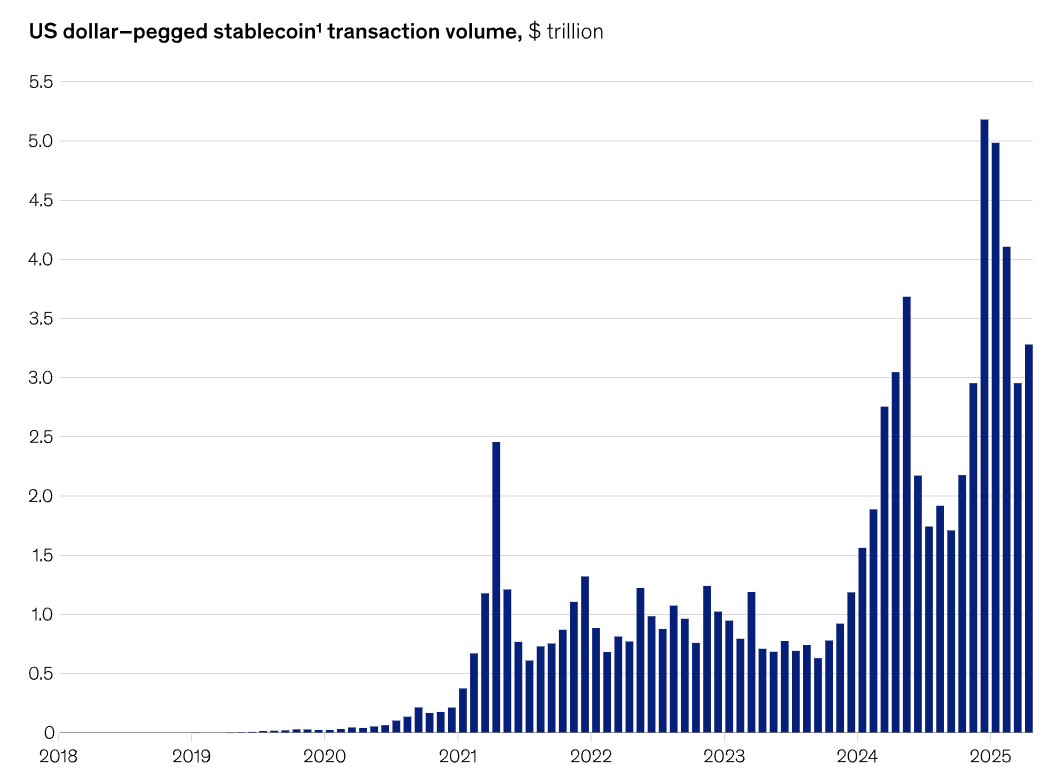

From January to July 2025, transaction volume, that is, the total amount of money moved using stablecoins, rose 83% compared to last year, reaching over five trillion dollars. Some of this activity comes from computers automatically trading back and forth extremely fast, but even if you remove that, regular everyday use still adds up to about one trillion dollars — more than double last year.

Source: McKinsey

The balance of stablecoins in circulation, which is the amount of stablecoins actually held out there, has also grown fast. In August 2024, there were about $159 billion worth of stablecoins in use. By August 2025, that number jumped to $250 billion, with most of that coming from the two biggest stablecoins: USDT and USDC. During this same time, about 30% of all crypto transactions involved stablecoins, showing that they are becoming one of the main ways people move money around in digital markets.

While stablecoins have already seen tremendous growth, there are three trends for stablecoins that have recently kicked off which warrant the attention of retail investors. All of them surround a massive integration shift: integration into global payments, institutional finance and even US Treasury markets.

More Countries, More Money

The biggest driver of stablecoins is globalization. As the world’s economy is more connected than ever, demand rises for a fast, cheap way to send money across borders — a demand stablecoins satisfy.

Normal international payments (like wiring money overseas) can take several days to arrive, charge high fees, especially foreign exchange (FX) fees and use complicated banking systems like SWIFT. Stablecoins are different: you can send them in minutes, and the fee is often less than 1%. A great example is remittances, that is, money that overseas workers send back home to support family. These transfers often cost over 6% in fees using traditional services. With stablecoins, people can send money almost instantly for far cheaper. For workers in the US sending money to Mexico specifically, stablecoins already make up 5-10% of all transfers, and experts think they may reach 30% within 3-5 years.

Stablecoins are also growing because the world relies heavily on the US dollar, which is the main currency used for global trade. Right now, about $15 trillion worth of US dollars are used outside the United States — a number that will likely increase as international trade and financial markets grow with more globalization. In many developing countries, it’s hard to access actual dollars or open a dollar bank account. But stablecoins like USDT and USDC are easy to get on crypto exchanges and apps. So people in places like Argentina (in 2023) used stablecoins as a safe, digital replacement for dollars when their local currency was unstable.

A Friend of Uncle Sam

Another driver of stablecoins is because financial institutions are embracing them. Earlier this year, the GENIUS Act was passed, which set clear rules to make stablecoins safer: most importantly requiring real dollar backing, liquidity standards and transparency. The newfound reliability and ensuing optimisms leads many people to believe the stablecoin market could grow massively and even be worth over three trillion dollars by 2030.

Stablecoins are especially becoming popular for business-to-business (B2B) payments Since early 2025, B2B stablecoin payments have grown 113%, and they now make up about two-thirds of all stablecoin activity. Big banks are also getting involved. Many leaders in finance say they already use stablecoins or expect to within the next three years, and global institutions are building their own stablecoin plans. A group of 10 major banks — including Bank of America, Deutsche Bank, Goldman Sachs and UBS — is exploring a multi-currency stablecoin. Meanwhile, 9 European banks are working on a euro-based stablecoin built on regulated systems. All of this shows that stablecoins are no longer just a niche crypto idea. Instead, they’re becoming part of the everyday financial system, used by real banks and companies around the world.

Credibility by Osmosis

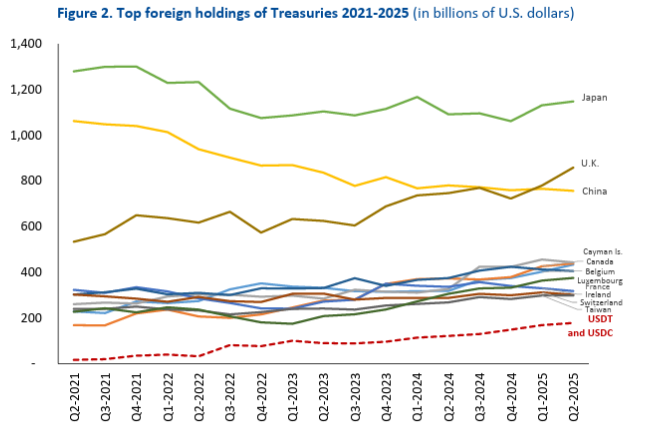

Stablecoins aren’t just popular with users but are also becoming deeply connected to other parts of the macroeconomy, especially the US government debt (Treasury) market. Companies that issue major stablecoins, like Tether and Circle, keep back over 80% of their reserves with short-term US Treasuries, becoming critical buyers of US government bonds. By the end of 2024, Tether alone owned about $94.5 billion worth of US Treasuries, which is close to 1% of all US debt held by foreign countries. From early 2024 to early 2025, stablecoins as a whole became the third-largest buyers of US Treasuries, with only the Cayman Islands and Belgium buying more. If stablecoin growth continues, they could soon become a key source of funding for the US government. Stablecoin issuers' role in the US Treasury market means stablecoins are gaining more legitimacy and importance, thereby giving regulators, investors and financial institutions even more reason to support them as they continue to expand.

Source: Brookings Institution

What to Consider

The above trends show how stablecoins are moving into the spotlight, away from being simply a speculative crypto niche. As regulation matures, cross-border adoption accelerates, and multinational firms increasingly integrate stablecoins into payments, the entire stablecoin ecosystem — issuers, exchanges, fintechs, banks, remittance companies and liquidity providers — should be considered by retail investors. You may consider:

- Crypto exchanges enabling stablecoin trading and custody:

- Coinbase (COIN)

- Nasdaq (NDAQ)

- Fintech payment platforms incorporating stablecoins into transfers and remittances:

- Block (XYZ)

- PayPal (PYPL)

- Global card networks piloting stablecoin and token-based settlement:

- Visa (V)

- Mastercard (MA)

- Mining companies maintaining the security backbone that stablecoins rely on:

- Riot Platforms (RIOT)

- Marathon Digital Holdings (MARA)

- Public companies with direct balance-sheet exposure to crypto assets:

- MicroStrategy (MSTR)

- Enterprise technology enabling tokenization and stablecoin settlement for institutions:

- IBM (IBM)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.