Parents

Research

Feb 25, 2026

Biofuels: The Lesser Known Hero of the Green Energy Transition

Andrew Z

Research Fellow

Biofuels: The Lesser Known Hero of the Green Energy Transition

The Key to a Greener World

Biofuels play a critical role in the global push to cut emissions. In the United States, biofuel production has been rising steadily since the early 1980s, mostly because of government policies and overarching movement to reduce reliance on fossil fuels. Biofuels are liquid fuels made from feedstocks: plants, waste oils and other biological materials. Most biofuels are used for transportation, such as blending into gasoline or diesel.

In 2022, the United States produced about 18.7 billion gallons of biofuels, split across four categories set by the Energy Information Administration (EIA). Ethanol was by far the largest, accounting for about 82% of total U.S. biofuel production and roughly 75% of consumption, mainly because it is blended into gasoline used by everyday drivers. Biodiesel made up the second-largest share at around nine percent of production and consumption, and is typically blended into petroleum diesel. Renewable diesel, which can fully replace fossil diesel without changing engines or fueling systems, also accounted for about eight percent of production and nine percent of consumption, and has been growing much faster than other biofuels. The remaining share came from other biofuels, such as renewable jet fuel (also known as sustainable aviation fuel, or SAF), renewable heating oil and biojet fuel, which together still represent a small portion of total volume but are expected to grow as harder-to-electrify industries push to cut emissions.

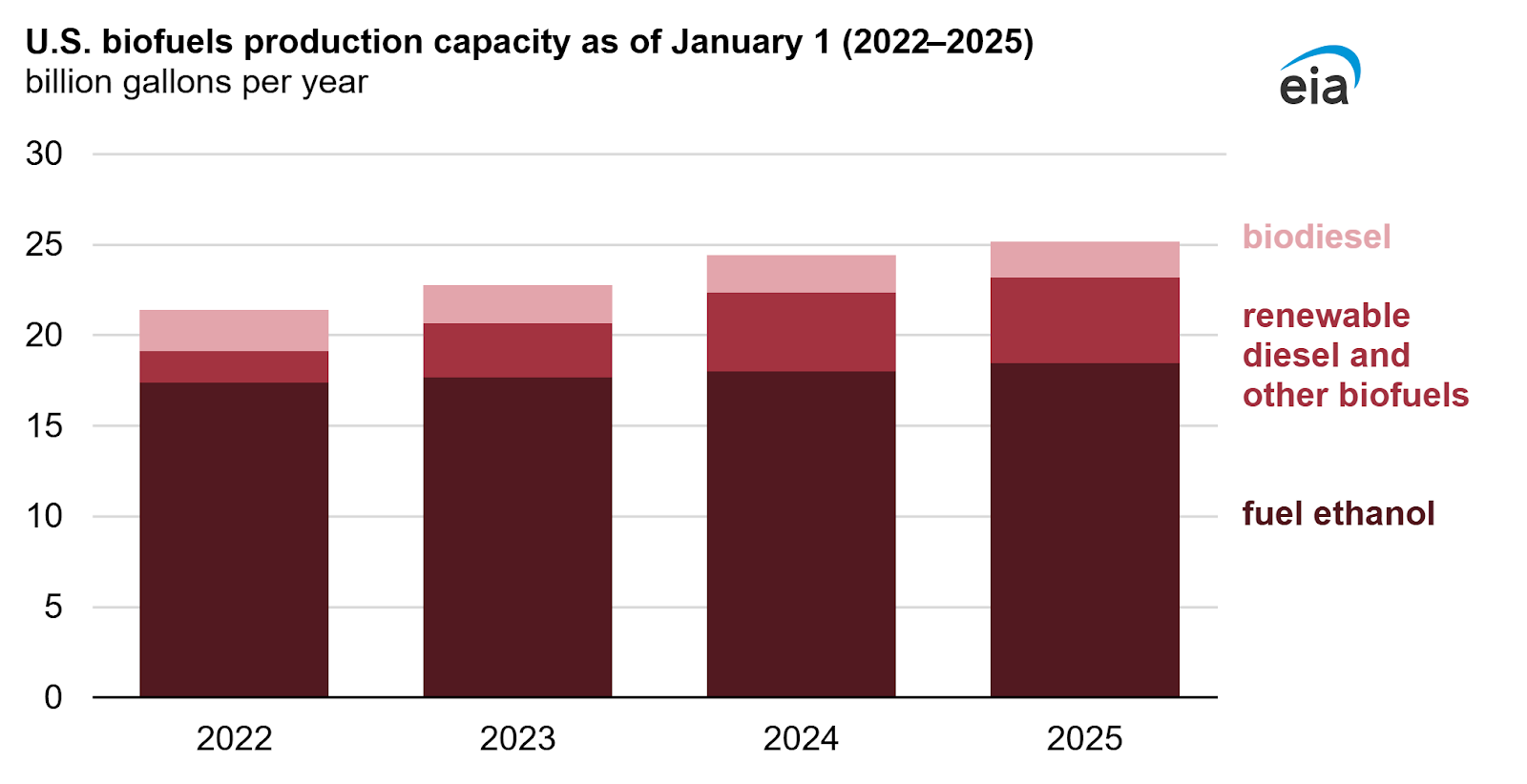

Total US biofuel production capacity rose from just over 21 billion gallons per year in 2022 to about 25 billion gallons per year by 2025. However, the pace of new capacity began to slow in 2024, increasing only three percent from 2024 to 2025. Biofuel plants require large amounts of feedstocks, capital, and time to build, which limits how quickly supply can respond.

Source: Energy Information Administration

While production of biofuel faces constraints, three trends will reshape the biofuel industry: critical industries are resorting to biofuels out of necessity, biofuel production is overcoming its own flaws (namely carbon emission) and the world is recognizing the importance of sustainable aviation fuel (SAF).

Electricity Can’t Save You

Biofuel has a unique ability to provide clean energy to sectors that electricity — another major channel — can’t reach. Unlike EVs or homes, some products and industries, especially those requiring long range, heavy loads and high energy density, can not be powered by electricity. Accordingly, aviation, maritime shipping, heavy trucking and parts of industrial heat are all “hard-to-abate” sectors. These sectors rely on liquid fuels because they pack far more energy into less weight and volume.

These industries are massive providers of biofuel demand. Biofuels are one of the few scalable replacements for fossil fuels because they can first be blended with conventional jet and marine fuels, thereby functioning without any new infrastructure requirements. Today, biofuels make up about four percent of global transport energy use, but their role is set to expand rapidly.

Consider aviation. No battery today can power a long-haul or transcontinental flight, making electrification unrealistic for commercial air travel. As a result, sustainable aviation fuel (SAF), a type of biofuel, is currently the only viable pathway to significantly reduce emissions from long-distance air travel. Demand for SAF is expected to grow fivefold by 2030, driven in large part by mandates such as the European Union’s ReFuelEU program and the International Civil Aviation Organization’s CORSIA framework. Or similarly for heavy-duty trucking and maritime trade, long-haul trucks and large ships still depend heavily on diesel because of weight, charging time and range limitations. With the absence of sufficient battery or hydrogen technologies, renewable diesel and other biofuel blends offer one of the only practical ways to cut emissions immediately.

Together, aviation and shipping are expected to account for more than 75% of new global biofuel demand by 2030, as both industries work toward net-zero emissions targets by mid-century. In aviation alone, global biofuel demand is expected to reach 2.0-7.8 exajoules by 2050, compared with about 4.3 exajoules of total biofuels produced worldwide today, suggesting that future demand could exceed current global supply by a wide margin. More broadly, modern bioenergy's contribution to final energy demand, including electricity and heating, is currently about four times larger than the combined contribution from wind and solar electricity. As the clean energy transition pushes into sectors that electricity cannot reach, biofuels are increasingly demanded as not just a complementary solution, but a necessary one.

Biofuels Aren’t Perfect?

Improvements in biofuel production will allow the industry to overcome one of its biggest hurdles: carbon emission. On average, global biofuels production actually emits about 16% more carbon dioxide than the fossil fuels they replace, mainly due to the feedstock used.

For much of the past two decades, first-generation biofuels were made from food crops like corn, sugarcane, soybeans and palm oil. These fuels benefited from mature supply chains and low costs, but they also created trade-offs. Using food crops for fuel can compete with food production and has been linked to land-use change and biodiversity loss. These concerns limited how far first-generation biofuels could scale on their own.

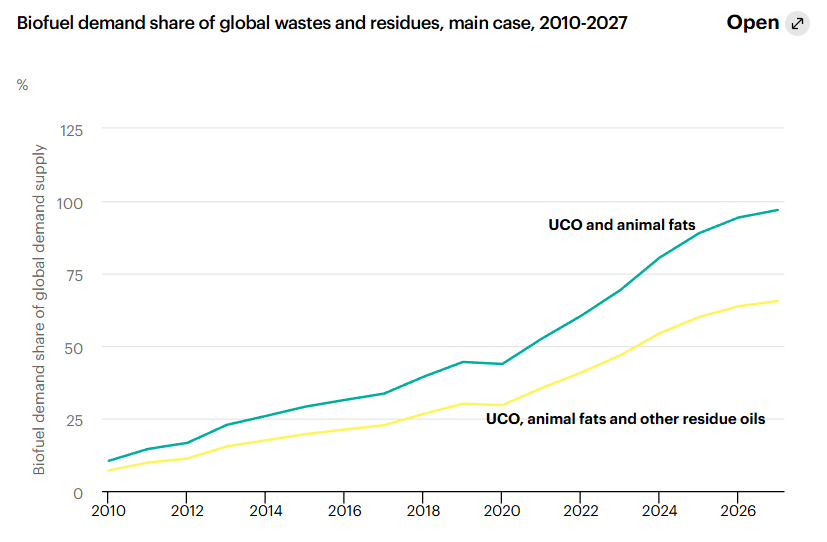

The industry is now shifting toward second-generation biofuels. These fuels use non-food, circular feedstocks, such as agricultural residues, forestry byproducts, used cooking oil, animal fats and even municipal waste. Because they rely on materials that would otherwise be discarded, they largely avoid land-use conflicts and can reduce lifecycle emissions by more than 80% compared with fossil fuels. This shift is evident: Many US and European biofuel refineries have been retrofitted to process waste-based inputs, and in some facilities, used cooking oil, tallow, and residues now account for more than 60% to 80% of total feedstock use. Thus, waste and residue feedstocks are projected to account for about 13% of global biofuel production in 2027, up from 9% in 2021, reflecting both policy support and strong market demand.

Source: Information Energy Administration

Looking further ahead, producers are also working to responsibly expand feedstock supplies. Additional sustainable crop-based feedstocks, when managed carefully, could support another 8.5 exajoules of biofuel production, or roughly 300 billion liters, compared with about 4 exajoules, or 160 billion liters, produced in 2021. In other words, even without radical breakthroughs, improvements in feedstock sourcing and sustainability practices could support nearly a 70% increase in global biofuel production by 2030.

Together, these changes make biofuels more politically acceptable, more attractive to customers and better positioned to meet growing demand from industries that need low-carbon liquid fuels.

To the Skies

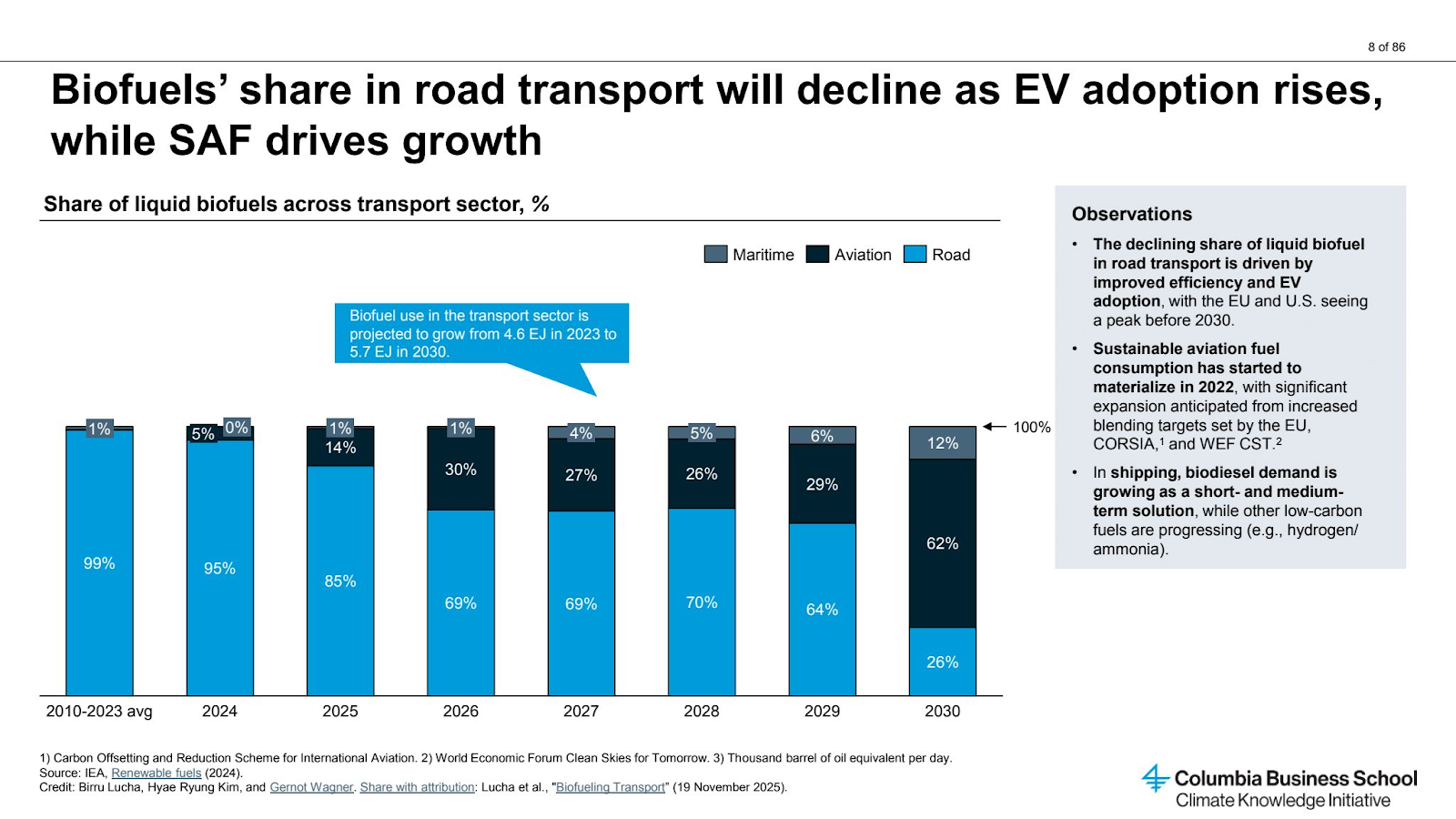

As mentioned earlier, aviation is one of the hardest industries to decarbonize, making biofuels widely viewed as the only realistic near-term option for cutting emissions from commercial aviation. One specific biofuel designed to replace petroleum jet fuel is sustainable aviation fuel (SAF), which has been the shining star of biofuels starting in late 2024.

Source: Columbia Business School

Even though SAF still represents a small share of total jet fuel use, production is ramping up quickly. From December 2024 to February 2025, US production of the EIA's “other biofuels” category (which is dominated by SAF) doubled. SAF production specifically grew from 25,000 b/d in late 2024 to around 30,000 b/d in May 2025, supported by growing airline demand and policy mandates that require increasing SAF blending over time.

What makes SAF especially powerful as a growth driver is the rise of “drop-in” ability. Unlike traditional biofuels that must be blended with fossil fuels to work, drop-in fuels can be used directly in existing aircraft, pipelines, refineries and fueling systems, enabling SAF to be scaled and emissions to be reduced much faster. As global air travel continues to grow, demand for these high-energy liquid fuels will grow alongside it.

Most SAF produced in the United States today are hydroprocessed esters and fatty acids (HEFA), a type of drop-in fuel. HEFA uses vegetable oils, waste fats, and used cooking oil as inputs and relies on similar equipment to renewable diesel plants, which already operate at commercial scale. This has helped SAF production get off the ground quickly and at lower capital cost than other advanced biofuel technologies. However, HEFA-based SAF faces a key limitation: feedstock availability and cost. Inputs like soybean oil are limited and expensive, with wholesale prices around $3-$4 per gallon in 2024, compared with $2-$3 per gallon for petroleum jet fuel.

That pressure is driving investment in alternative drop-in pathways such as alcohol/ethanol-to-jet (ETJ) and Fischer-Tropsch processes. These technologies expand the range of usable feedstocks to include ethanol, agricultural residues and other alcohols. ETJ is especially important because it builds on existing ethanol production, which is abundant and often cheaper than HEFA feedstocks. The technology to convert ethanol into jet fuel is still early: Commercial SAF production using ETJ began in 2024 with LanzaJet’s Freedom Pines Fuels. But it is expected to scale through 2030 and beyond, with 15 ETJ production facilities announced as of 2025.

SAF’s rising importance and the broader development of drop-in fuels are expanding the reach of biofuels. Demand from aviation is accelerating quickly, and technological improvements will support supply, ultimately sustaining growth in the biofuels industry.

What to Consider

The increasing reliable demand from hard-to-electrify industries, the ability to scale sustainable feedstocks and the feasibility to create drop-in fuels to be deployed easily into existing energy systems are trends making biofuels more attractive to retail investors. Investors may consider:

- Companies focused on making next-generation biofuels like SAF

- Gevo (GEVO)

- Companies turning biofuels into usable transportation fuel at scale

- Valero (VLO)

- Chevron (CVX)

- ExxonMobil (XOM)

- BP (BP)

- Companies supplying the raw materials used to make biofuels

- Archer-Daniels-Midland (ADM)

- Darling Ingredients (DAR)

- Companies that move fuels through pipelines and storage networks

- Enbridge (ENB)

- Companies building fueling networks for low-carbon fuels

- Clean Energy Fuels (CLNE)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.