Parents

Research

Mar 4, 2026

The Hidden Winners in a Slowing Construction Industry

Andrew Z

Research Fellow

The Hidden Winners in a Slowing Construction Industry

The Industry Behind it All

Behind all buildings and physical spaces is the construction industry. For investors, one especially important segment is nonresidential construction, which covers buildings used by businesses and institutions. This part of the industry includes commercial buildings like offices where people work; warehouses and logistics centers that support e-commerce; manufacturing buildings like factories; and institutional buildings such as hospitals, schools and government facilities. Because these projects are funded by companies and public budgets rather than individual homebuyers, changes in nonresidential construction often reflect broader economic trends, such as business investment, technological shifts and government spending priorities.

In 2025, however, tariffs have raised the price of imported materials, labor shortages have made projects more expensive, interest rates remain high and government spending cuts have limited public projects: all of which slowed recent US construction momentum. While the industry began 2025 with solid growth, spending started to weaken as the year progressed. By the second quarter, total construction output reached $1.732 trillion, a 0.6% fall. By July, overall construction spending declined nearly three percent year over year, mainly due to drops in commercial and manufacturing projects.

Source: Deloitte

Nonresidential building construction in particular has also underperformed earlier expectations. Forecasters had projected spending to rise by almost two percent for 2025, followed by a similar increase this year. Instead, estimates now suggest commercial construction fell roughly three percent, manufacturing dropped closer to five percent, and institutional construction, which had been expected to grow about six percent, expanded at less than half that pace. Looking ahead, analysts expect only modest gains, with nonresidential building projected to increase around 1 percent this year and about 2.2% in 2027. Because these figures are not adjusted for inflation, actual growth could be even weaker once higher material and labor costs are considered.

However, construction should not be overlooked. It remains one of the largest industries in the world, worth about $13 trillion in 2023 alone or roughly seven percent of total global output. Within its existing stature, construction is being redefined in three areas: a shift toward data center construction, evolution in healthcare construction and the implementation of AI to fix one of construction's most persistent problems. All of these trends should fuel interest in construction among retail investors.

The Obvious Survivor: Data Centers

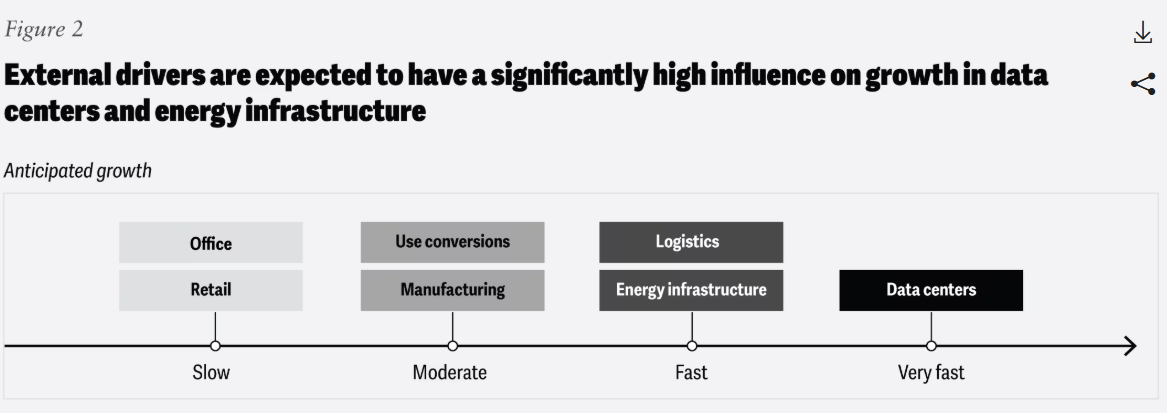

While the overall outlook for nonresidential construction has been modest, not every segment is moving in the same direction. One clear area of strength is data center construction. This area is largely driven by the rapid adoption of AI and the continued growth of cloud services. Training and running AI models requires massive computing capacity, which in turn requires larger data centers with more servers, larger facilities and significantly more electricity.

Source: Deloitte

Data centers, once considered a niche category, are becoming one of the most demanded, energy-intensive and capital-intensive forms of construction. Power usage from US data centers could increase more than fivefold by 2035, rising from 33 gigawatts in 2024 to roughly 176 gigawatts. At that level, data centers alone could account for most of the country’s incremental electricity demand, potentially adding more than 123 gigawatts to the grid.

Spending trends reflect the pivot to data centers. Construction spending on data centers increased by an estimated 32% last year, and forecasters expect additional gains of about 26% this year and nearly 17% in 2027. Federal policies supporting re-shoring have furthered this growth. The emphasis on data centers is not limited to the centers themselves: It points to a broader ecosystem that includes land development, power generation, cooling systems, networking equipment and specialized contractors. As computing demand continues to expand, these supporting pieces of infrastructure are increasingly shaping where construction will be in demand.

The Older the Better

While not as well known as data centers, healthcare construction is another segment that has remained relatively resilient even as other parts of nonresidential building have slowed. Despite cutbacks in key health care funding programs, spending on health care facilities still posted a modest increase of about 1.5% last year, a number expected to surge in 2026 and beyond. Current forecasts project spending on health care facilities to rise just over 4.6% this year and by an additional four percent in 2027.

Construction brojects are expected because healthcare is increasingly coming from smaller and more distributed facilities rather than large, centralized hospital campuses. Ambulatory care, which includes outpatient visits and same-day procedures, now accounts for about 30% of total provider revenues and continues to trend upward. At the same time, medical buildings make up over 40% of all health care construction, highlighting how much investment is shifting toward physical infrastructure that supports these services.

This change reflects a broader shift in how and where care is delivered in response to forces in healthcare. Staffing shortages, advances in medical technology and patient preferences for receiving treatment closer to home are encouraging health systems to move away from the traditional “big hospital” model. Instead, care is becoming more decentralized, with ambulatory surgery centers, cancer treatment facilities, medical office buildings and urgent care clinics located throughout communities. These smaller facilities must often be built faster and more efficiently while still meeting strict clinical and safety standards, which changes the way projects are designed and executed. Furthermore, the aging population is an underlying tailwind for demand for healthcare facilities.

To meet these demands, construction methods are also evolving. Prefabrication, sometimes called modular or off-site construction, is increasingly becoming the new standard for hospital design. Components such as patient rooms, bathrooms, building exteriors, and even mechanical and electrical systems are assembled in factories and then installed on site. This approach can shorten construction timelines, improve quality control, and reduce disruptions around active medical campuses. It also helps address persistent labor shortages (which will be discussed in the following section) by allowing more controlled and efficient work environments.

Healthcare construction will thus flourish, shaped not just by higher demand for services but along with structural changes in how care is delivered and improvements in how facilities are built.

Maybe Automation Isn’t Bad?

One of the most persistent challenges facing construction is a labor shortage. Construction is projected to need about 499,000 new workers by 2026, with roughly 439,000 additional hires required in 2025 alone. If these positions remain unfilled, the industry could lose nearly $124 billion in construction output. Structural factors suggest the problem may worsen. By 2031, about 41% of construction workers are expected to retire, while only around 10% of current workers are under age 25. At the same time, fewer young people are entering the trades, with only about seven percent of potential job seekers expressing interest in construction careers. Competition for skilled labor is also increasing as engineering talent shifts away from traditional building toward technology firms and large projects in areas such as data centers, energy storage and semiconductors draw workers. Immigration has historically helped fill these gaps. Of the roughly 12 million payroll and nonpayroll workers in construction, about 25% are foreign-born. An estimated half of these foreign-born workers are undocumented, leaving the labor supply vulnerable to changes in immigration enforcement and policy.

Source: McKinsey

But a way to maintain productivity lies in the fact that construction remains one of the least automated major industries, relying heavily on manual, on-site labor. As wages rise and schedules tighten, firms are increasingly turning to technology to maintain productivity and control costs. AI-driven scheduling systems can automatically coordinate tasks, anticipate disruptions, and adjust timelines in real time. Computer vision and safety analytics use cameras to detect hazards and improve compliance, helping reduce accidents on large sites. Digital workflows that integrate building information modeling, 3D printing, and digital twins allow teams to simulate projects before construction begins, improving accuracy and shortening timelines, in some cases by up to 20 percent. Connected sensors and Internet of Things devices track equipment usage and predict maintenance needs, while autonomous machinery and robotics are gradually automating repetitive or hazardous tasks.

Adoption is already underway. About 60% of construction firms report using some form of AI, though this is concentrated in large companies. Spending on AI technologies by construction companies is expected to nearly triple in the coming years, rising from about $4.96 billion in 2025 to roughly $14.72 billion in 2030. Rather than replacing workers entirely, these tools allow firms to do more with limited labor, and transfer the knowledge of the finite amount of skilled workers once they retire, thereby aiding construction companies against labor supply problems.

What to Consider

While construction may not be as momentous across the board, the industry still warrants the attention of retail investors. Trends in certain areas like data centers and decentralized healthcare facilities are paving the way for construction’s growth — a growth supported by productivity gains from AI-enabled construction technologies in the face of labor shortages. You may consider:

- Companies supplying heavy equipment used across data centers, hospitals, and large infrastructure projects

- Caterpillar (CAT)

- Deere & Company (DE)

- United Rentals (URI)

- Companies tied to building systems required in data centers and modern facilities

- Johnson Controls (JCI)

- Trane Technologies (TT)

- Carrier Global (CARR)

- Honeywell (HON)

- Companies exposed to engineering services, construction management and complex project delivery

- Emerson Electric (EMR)

- Companies benefiting from broad residential and nonresidential building activity

- Lennar Corporation (LEN)

- PulteGroup (PHM)

And you can get invested in these through a custom portfolio created by Bloom:

Disclosure: This material is provided for informational purposes only and is not intended to constitute, and should not be relied upon as, investment advice, a recommendation, or a solicitation to buy or sell any securities. Nothing contained herein is intended to be, or should be construed as, an offer to sell or a solicitation of an offer to purchase any security or investment product. Any investment decisions should be made only after careful consideration of the applicable risks and, where appropriate, consultation with qualified financial, legal, or tax professionals.